A field guide to the agentic commerce protocol alphabet soup. What each one means, what each one does, which ones aren't protocols at all, and the one layer that's yours no matter who wins. Current as of June 2026.

If you read the trade press right now, you might think a format war broke out. ChatGPT can check out. Google shipped a Universal Cart. Visa and Mastercard each launched an agent payment scheme within months of each other. Stack the acronyms — ACP, UCP, AP2, MCP, A2A, ATP — and it reads like VHS versus Betamax, with your catalog as the bet.

It isn't. It's a vertical stack, not a horizontal format war. Most are built to layer on top of one another, and several of the names getting cited in the same breath aren't commerce protocols at all. The useful question was never which standard wins. It's which layer each one touches — and which layer stays your responsibility regardless of the outcome.

Sort them by layer and the war dissolves into a division of labor.

The protocol stack, top to bottom

There are five layers in play. Almost every protocol you've heard about lives cleanly in one of them. The confusion comes from treating them as peers when they're actually a vertical.

Agent plumbing

MCP (tool access) and A2A (agent-to-agent delegation). Not commerce protocols. This is the substrate that lets an agent use tools and talk to other agents. MCP in particular gets dragged into commerce conversations constantly — it's how an agent reaches a commerce protocol, not the protocol itself.

Commerce orchestration

The discovery-to-checkout-to-post-purchase flow. ACP and UCP live here. This is the only layer with a genuine two-camp dynamic.

Payments and authorization

How money moves and how the system proves the user actually authorized the purchase. AP2 lives here, alongside the card-network schemes.

Identity and trust

Whether the agent at your checkout is a credentialed actor or an anonymous bot, and whether it's carrying real instructions. Visa's Trusted Agent Protocol lives here.

Product data

The catalog the agent reads at every step above. No protocol on this list generates or manages it.

The two that actually orchestrate commerce

This is the only layer where "rival camps" is a fair description — and even here, they interoperate through shared building blocks.

ACP — Agentic Commerce Protocol

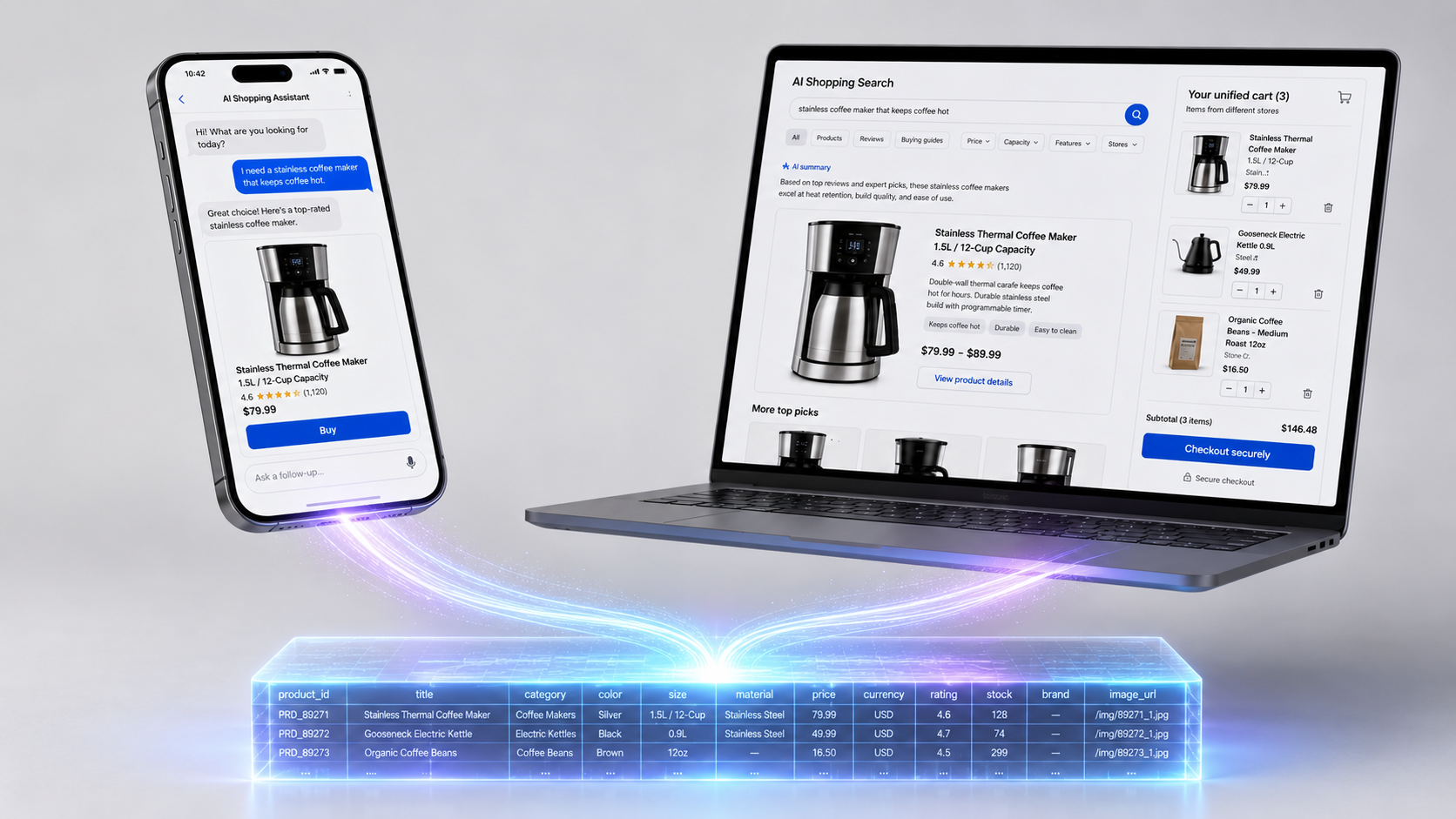

Co-developed by OpenAI and Stripe, with Meta now involved. Announced in late September 2025, it powers Instant Checkout in ChatGPT, launching with Etsy sellers and Shopify merchants. The design preserves the things merchants care about: you remain the merchant of record, orders flow into your existing backend, you charge the card, you handle tax, fulfillment, and returns. ChatGPT carries the wallet and finds the product; the sale is still yours. Under the hood it works by passing a secure payment token between the buyer, the agent, and your business.

UCP — Universal Commerce Protocol

Google's, co-developed with Shopify, Etsy, Wayfair, Target, and Walmart, with checkout features that rolled out in early 2026. It spans the full journey — discovery, checkout with pricing and tax, payment, and post-purchase support — and powers the Buy button in AI Mode on Search and in Gemini, plus the new Universal Cart that consolidates items across retailers. It connects to your store through the native_commerce product attribute in Merchant Center, and it's explicitly built to work with A2A, AP2, and MCP.

The honest comparison: different surfaces, same merchant-of-record principle, both leaning on shared payment-token plumbing. ACP reaches buyers inside ChatGPT. UCP reaches them inside Google's AI properties. Merchants do not choose between them, just as you do not choose between Google Shopping and Meta ads. You decide which surfaces you want to be buyable on, and you adopt what each one requires.

The payments layer, and why the card networks aren't a fourth and fifth standard

AP2 — Agent Payments Protocol

Google's, announced September 2025 with 60-plus launch partners. It's open, vendor-neutral, and payment-agnostic — cards, bank transfers, and stablecoins via its x402 extension. The idea worth understanding, because it's the genuinely new one, is the mandate: a cryptographically signed credential that proves what the user authorized. AP2 defines an Intent Mandate (what the user asked for), a Cart Mandate (the priced, line-itemed order the merchant returns), and a Payment Mandate (the authorization to charge). Together they answer the three questions that break when a human isn't clicking Buy: did the user authorize this, does the request reflect their actual intent, and who's accountable if it goes wrong.

The network schemes

Mastercard Agent Pay issues Agentic Tokens off its existing tokenization service — a card credential scoped to a specific agent, a specific merchant, and a specific consent policy, so the agent never holds the raw card number. Visa runs Intelligent Commerce on the same idea. Here's the part that cuts the confusion: these expose tokenized card credentials that act as the funding instrument inside an AP2 Payment Mandate. Visa and Mastercard were both at the UCP table, and both were named in Stripe's shared-payment-token work. They aren't competing standards stacked beside AP2 and UCP. They're the rails running underneath them.

The acronyms that aren't peers

This is the section nobody writes, and it's the one that keeps you from getting jumbled. Not every acronym in a LinkedIn post is a commerce protocol, and treating them as equivalent is how the whole picture goes blurry.

- MCP is the tool layer. It standardizes how an agent calls external tools and functions. It is not a payment or checkout protocol, and it gets miscited as one roughly every week.

- A2A is agent coordination — how one agent delegates to another. Also not commerce. Both MCP and A2A are the floor the commerce protocols are built on, not alternatives to them.

- ATP is the trap. In the agentic-shopping context, there's no major-player protocol behind those letters. Depending on who's typing, "ATP" is usually a mislabel of Visa's Trusted Agent Protocol — which is real, and which lives at the identity-and-trust layer, letting a merchant verify that an agent at checkout is credentialed and authorized rather than a scraping bot — or it's one of several small agent-economy projects (an "Agent Transaction Protocol," sometimes ATXP) built for agent-to-agent micropayments and governance, not consumer checkout. Knowing the difference is the difference between mapping the architecture and repeating a press release.

What every one of these has in common

Walk back up the stack and a pattern shows up that none of the announcements lead with.

ACP needs a clean product feed to put your items in front of a ChatGPT buyer. UCP won't render a Buy button until the native_commerce attribute is populated correctly in Merchant Center. An AP2 Cart Mandate is a cryptographic signature wrapped around your pricing and line items — it is exactly as accurate as the catalog data underneath it, and not one degree more.

None of these protocols clean, structure, or validate your catalog. They read it and transact on it, at machine speed. That's the layer with no logo and no launch event, and it's the one that's been yours the whole time.

The shift agentic commerce actually introduces isn't the disappearance of the data layer. It removes the delay between a bad data feed and a lost transaction. A wrong price or a stale inventory count used to surface as a disapproval in a queue, or a soft dip in performance you could diagnose next week. In an agent-mediated checkout, the same error surfaces as a failed transaction or a sale completed on the wrong terms — immediate, transactional, and propagating as fast as the protocol moves. The protocols got faster. They did not get more forgiving.

What a merchant does about it now

Resist the urge to integrate "a protocol." Here's the work that holds up regardless of which standard pulls ahead:

- Decide which surfaces you want to be transactable on. ChatGPT via ACP, Google's AI surfaces via UCP, more arriving. This is a business decision about where your buyers are, not an engineering one.

- Audit your catalog against what these protocols assume. Accurate real-time pricing and inventory, valid variant structure, correct product identifiers, current compliance status, and the specific attributes each surface requires — native_commerce for UCP, complete feed data for ACP.

- Treat it as the discipline you already run, with the stakes raised. This is the same catalog integrity that governs feed health on Google, Meta, and Amazon today — now enforced at transaction speed, where the failure mode is a bad purchase instead of a fixable disapproval.

This is our core architecture. GoDataFeed acts as your centralized routing engine, not a passive spreadsheet. We sit between a single catalog and every AI surface — structuring the data, validating it against the surface's rules, and optimizing what the product says when it arrives. So whatever reads the catalog — a Shopping auction, a Performance Max bid, or an AI agent completing a checkout — works from your commercial logic instead of a best-effort guess. For the deeper version of how that maps to agentic commerce specifically, see [UCP explained: what agentic commerce requires from your product data].

The part that outlasts the logos

The standards are converging faster than any single post can track. Visa's protocol has already been aligned to work with OpenAI's. UCP is built to ride on AP2. The card networks are plugging into everything. A year from now the brand names on the slides may have reshuffled.

The layer model won't. There will be a surface where buyers discover products, an orchestration layer that runs the checkout, a payments layer that moves the money and proves consent, a trust layer that screens the agent, and — underneath all of it — the product data every one of those layers depends on and none of them generates.

Stop tracking protocol updates and start treating your product data as your primary transactional API.

Bryan Falla

Bryan is a digital marketer with roots in journalism and creative writing. Over the past decade, he's helped hundreds of online retailers develop and implement ecommerce marketing strategies. When he isn't educating retailers on ecommerce, he's out exploring South Florida and stalking local breweries.

.png)

.png)