Millennials and Gen Z shoppers are rapidly taking over as the primary spenders in the economy. However, these groups are much more reluctant to make impulsive purchases or stretch themselves thin financially. Additionally, credit card applications are down – especially those who have been previously denied.

All these variables add up to a major consumer group that’s wary of making large online purchases and, in some cases, unable to – even if they wanted to. With high-priced items subsequently moving into the ecommerce space, there’s trouble on the horizon for shoppers unable or unwilling to make big purchases outright.

But there is a solution: point of sale financing.

This new frontier of online payments – also known as consumer financing or consumer credit – is the happy medium between price-minded shoppers and big-ticket online purchases.

Aversion to credit cards

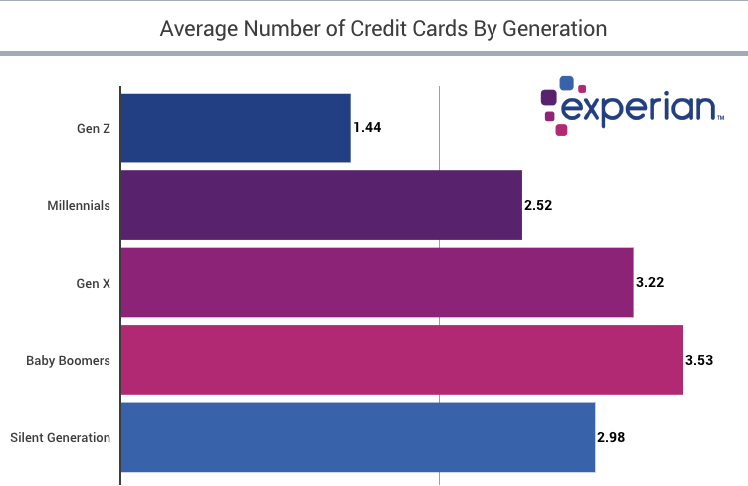

Too many Millennials have seen what credit card debt can do to those trapped under it. Their parents (Baby Boomers in most cases) have accumulated more credit card debt than any other generation. Most Millennials and Gen Z shoppers have seen and heard the cautionary tale of credit cards.

Younger consumers who do have credit cards are still using them for big purchases but paying them off faster and not racking up as much debt. As a result of self-imposed spending limits, bigger purchases are few and far between for these shoppers. But the demand is still there. That’s why pay-as-you-go plans, installment plans and checkout financing are all on the rise.

These payment options offer the same convenience as credit cards – get the item now and pay later – without the threat of high APR and big upfront spending costs. Shoppers are much more open to spending $2,000 on a 12-month installment plan than charging it upfront and dealing with overhanging credit card debt.

Reasonable debt

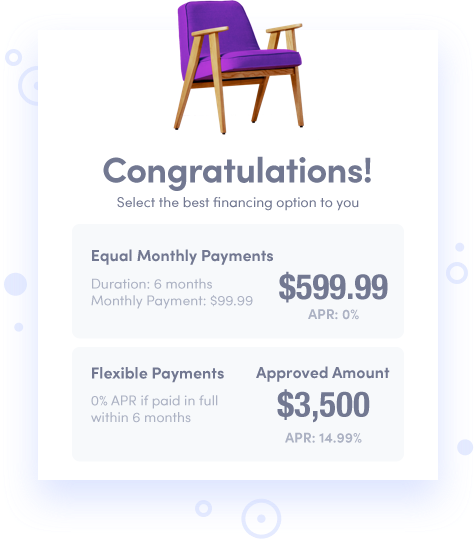

The concept of consumer point of sale financing is appealing for more reasons than just avoiding a big upfront charge. It doesn’t have the stigma of credit card debt, or the compounding interest that comes with it. Borrowers know exactly how much they’ll need to pay on a checkout financing loan each month – it won’t rise or fall. Moreover, it’s a debt they can’t add to by swiping their card absent-mindedly.

In short, point of sale or checkout financing for consumer loans has become a staple of “reasonable debt.” Shoppers recognize it as debt, and understand the nature of it, but they’re more willing to take it on because they have control over it. They get to pick their terms and rate. They’re aware of their payments ahead of time. And, when the debt is closed it’s done with outright.

It’s the best of all worlds for consumers and retailers alike. Consumers get what they want upfront and agree to debt on their terms; retailers increase sales and accommodate a broader range of shoppers.

Smarter payments for responsible consumers

Modern consumers are smart. They’re not going to stretch themselves thin for something they don’t need. That said, they are smart enough to assume debt they can handle for something they deem worthy of it. Demand will always be there; flexible financing options need to follow.

Millennials and Gen Z shoppers may clutch their wallets tighter, but they’ll loosen the purse strings if retailers meet them halfway. Point of sale and checkout financing and credit is the smarter payment option for today’s smart, responsible consumers.

Single lenders vs. multi-lenders

The world of checkout point of sale financing has a distinct split between “single lenders” and “multi-lenders.” To the consumer, this distinction is almost impossible to spot. For retailers, it makes a big difference. Single lenders vs. multi-lender platforms can have a huge impact on who gets approved for financing (or not), what terms are available and what sales will look like.

Single lenders

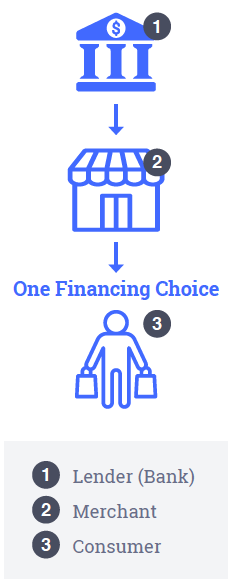

Single lenders typically focus on “prime” credit applicants. They’re after consumers with good to great credit, with the most favorable variables. This includes good credit history, high income and low to no existing debts.

These lenders – Affirm, Bread, and others – use specific credit underwriting terms to target consumers. Single lenders also act as banks and usually have one source of fund distribution. This means their risk is higher, which attributes to their focus on prime borrowers. Anyone not fitting the “prime” mold is usually denied, which means turning away ~70% of applicants to focus on the top ~30%.

There’s nothing wrong with this strategy for lenders, they’re simply targeting the people most likely to pay back their loans! For merchants, this impacts sales. Customers outside of the prime category may not qualify despite their clear ability to pay back their loans. Likewise, denied shoppers may abandon their cart altogether to shop elsewhere. As a result, abandoned carts skyrocket and conversion rates fall.

Multi-lenders

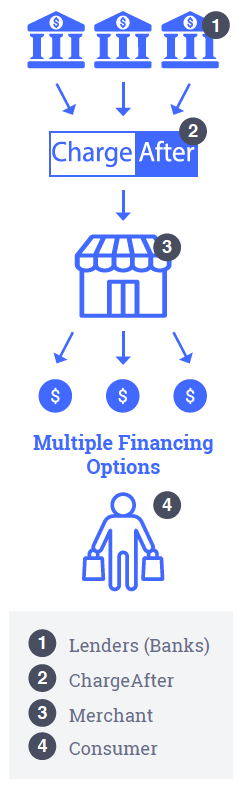

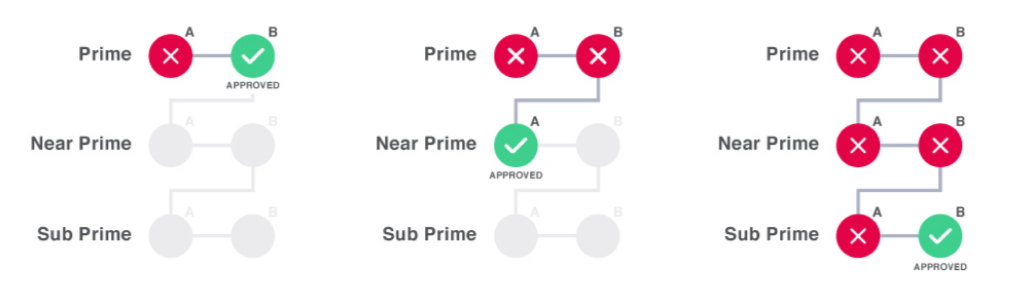

Multi-lenders like ChargeAfter use a network of lending options, funneled through a single user checkout experience. Customer data isn’t processed against a set of uniform terms targeted at prime applicants. Instead, it’s put through a “waterfall” of diverse lenders, with a variety of financing options provided to the consumer at approval.

The waterfall method is simple. A checkout financing application is checked against the prime lenders for approval, and if declined, it moves down to near-prime options. From there, sub-prime options are explored and so on, all the way down to lease-to-own financing options. All in a single application with results back in under 2 seconds on the merchant’s site!

Because multiple lenders are checked in the waterfall, different rates and terms are available to shoppers once approved, allowing them to pick the best personalized offer for them at checkout.

ChargeAfter approves up to 85% of applicants and provides personalized credit options for consumers to select from. More approvals, more options, more conversions!

The effect on ecommerce

As mentioned, denying a shopper access to financing can have disastrous results for abandoned carts, conversions and even customer loyalty. Conversely, giving borrowers more options with flexible repayment terms encourages confidence at checkout and results in higher AOVs and higher tickets.

More people are shopping online than ever before. Big-ticket items are more readily available, too. As a result, it’s in the best interest of online retailers to bring their customers diverse financing options to meet all credit types. Choosing a multi-lender platform means casting a broader net for interested shoppers and bringing in more sales.

In an age where it’s easier to buy an armchair online than going to a physical furniture store, ecommerce stores need the diversity multi-lenders offer. Not everyone has pristine credit, but that shouldn’t disqualify 70%+ of shoppers seeking sensible consumer loans.

About ChargeAfter

Founded in 2017, ChargeAfter’s platform was developed with the goal to help every shopper access fair financing options tailored to their unique needs.

ChargeAfter is a market leading financing platform that empowers retailers to offer consumers personalized financing options at checkout from multiple lenders. Through its growing network of global lenders, retailers can approve up to 85% of applicants in real-time and increase sales by up to 45%.

ChargeAfter’s network offers seamless integration for lenders to increase their customer base and compete for business while expanding into new retail markets by streamlining the distribution of credit into online and in-store point-of-sale financing.

ChargeAfter has offices in Tel Aviv, New York, and Sunnyvale to better support our global clients.

Jeffrey Tower

Jeffrey Tower is the VP of Marketing and Business Development at ChargeAfter. He has a rich background in ecommerce management as VP and director of ecommerce marketing in several IR Top 500 companies. Jeffrey also consults for several ecommerce SaaS technology companies and ecommerce merchants.